Mixed-Rate Mortgage

Would you like to combine the best of a fixed-rate and a variable-rate mortgage?

You'll have ten years at a fixed rate and the remaining years at a variable rate.

With bonuses¹

For salaries as from €2,000 net:

• APR in the first ten years of 3.00%

• APR in the remaining years of the Euribor rate+0.85%

• Variable AER of 4.18%

Bonus of 1.00 p.p.

For all other income:

• APR in the first ten years of 3.20%

• APR in the remaining years of the Euribor rate+1.00%

• TAE Variable 4.37%

Bonus of 1.00 p.p.

Opening commission 0.15 %

Variable AER calculated for an amount of €150,000 over 25 years.

Without bonuses²

For salaries as from €2,000 net:

• APR in the first ten years of 4.00%

• APR in the remaining years of the Euribor rate+1.85%

• Variable AER of 4.38%

For all other income:

• APR in the first ten years of 4.20%

• APR in the remaining years of the Euribor rate+2.00%

• Variable AER of 4.58%

Opening commission 0.15 %

Variable AER calculated for an amount of €150,000 over 25 years.

The best of both worlds

In the first 10 years of your mortgage loan*, enjoy the peace of mind of no interest rate changes. In the variable-rate period, you will benefit from a interest rate, which is calculated on the basis of the Euribor rate.

Up to 30 years

You can pay back the mortgage in up to 30 years. The sum of the oldest mortgagee's age and the mortgage's term may not exceed 75 years for a main residence and 70 years for a second residence.

Financing of up to 80%

You can finance up to 80% of your main residence and up to 70% of other homes. The amount to be financed will be the lower of the valuation and the purchase price.

How to get the Mixed-Rate Mortgage bonus

By subscribing Unicaja products and services, such as:

- Having your salary for an amount exceeding €600 a month directly deposited and credit card consumption.

- Home insurance, life insurance, temporary disability/unemployment insurance, health insurance, or car insurance.**.

- Contributions or balances in pension plans and/or investment funds.

A 5% discount at IKEA and a free decoration project with your Mixed-Rate Mortgage

Sign your Mixed-Rate Mortgage at Unicaja and give your home the welcome it deserves. Benefit from a 5% discount on any purchases exceeding €80 at IKEA (excluding decoration advice, transport, assembly and installation services).

In addition, if the purchase you make exceeds €500 you will also be entitled to a free decoration project.

Practical information on mortgages

Mortgage loan access guide

Here you can find the information you need to take out a loan for the purchase of a home.

Code of good practice

Here you have access to general information on measures to strengthen the protection of mortgagors

Fixed-Rate Mortgage

The Fixed-Rate Mortgage will give you the peace of mind of always paying the same repayment for your home.

Variable-Rate Mortgage

This is your mortgage if you are looking for an interest rate that adapts to the Euribor rate.

The Mixed-Rate Mortgage is used to purchase a home and is only available to natural persons who reside in Spain and have income and equity in euros. It is also necessary to open a current account at Unicaja and subscribe an indemnity insurance policy that covers any possible contingencies that may take place in the property. The mortgage's approval is subject to the institution's discretion and will be granted after a prior analysis of the risk's viability has been conducted.

The age of the Mixed-Rate Mortgage's mortgagee and the repayment term cannot add up to more than 75 years for a main residence and 70 years for a second residence (if there is more than one mortgagee, the age of the older mortgagee will be taken into account).

It is necessary to take out at least basic indemnity insurance to make sure that the mortgaged asset, which in this case is the home, is protected against any contingency.

By setting up an appointment at one of our branches. One of our managers will help you out there in a personalised way, informing you about your mixed-rate mortgage's monthly repayments and clearing up any doubts you may have.

If there are any errors in the data you have entered or you need to make changes to them, you can cancel the application and initiate a new one. When the manager gets in touch with you to process your application, you can also inform them about which data you wish to change and we will do it for you.

Variable AER (Annual Equivalent Rate), total cost of the mortgage loan and full amount owed by the mortgagee based on a typical example of a loan amounting to €150,000.00 having a front-end fee of 0.15% and a repayment term of 25 years through the payment of 300 constant monthly principal and interest repayments at the interest rate indicated below:

25-YEAR MIXED INTEREST RATE MORTGAGE

(1) Meeting all the requirements to obtain maximum interest rate bonus:

Variable AER with maximum bonus: 4.18 % (3). For salaries as from €2,000

This variable AER has been calculated pursuant to the provisions set forth in Act 5/2019 of 15 March governing real estate credit agreements.

- Annual percentage rate (APR): Fixed rate in the first ten years with bonus: 3.00%. Variable: One-year Euribor rate + 0.85% (half-yearly reviews). The last one-year Euribor rate value published in the Official Journal of the State of 02/07/2026 was 2.798%. The interest rate resulting from the sum of this value plus the above-mentioned differential is 3.65%. This APR can be obtained with other combinations of subscribed products/services other than those used by Unicaja to calculate the example.

- No. of monthly repayments: 300. Date the first monthly repayment is due: 05/08/2026. Repayments in the first ten years: € 711.52. Subsequently: € 744.10. Except for the last repayment of € 744.28. In order to calculate the repayments, total interest, total cost and the total amount owed as from the end of the fixed-rate period, the higher borrowing rate between the initial fixed rate and the reference index (one-year Euribor rate published monthly in the Official Journal of the State) plus the differential has been applied. The repayments have therefore been calculated by taking into account an APR of 3.65%. Nonetheless, we inform you that, as from the end of the fixed-rate period, the repayments' amount may vary depending on the variable interest rate to be applied.

- Total amount owed: € 240,647.33. Total interest: € 69,320.58. Total cost of mortgage loan: € 90,647.33.

Example of products selected by Unicaja, which can be jointly subscribed to obtain the bonified interest rate (APR) that has been used to calculate the variable AER with the maximum bonus:

Salary paid by direct debit from €2,000 net per month. Credit card consumption of at least €600, calculated in the 6 months prior to each half-yearly review date of the interest rate subsidies and at the opening of the loan Home protection insurance. Life Risk Insurance 100% associated with the loan. Minimum contribution to a Pension Plan of 0.6% of the outstanding capital in the 6 months prior to each half-yearly review date of the interest rate subsidies and at the opening of the loan.

Fulfilment of requirements will be checked as from when the loan is taken out and thereafter at successive half-yearly reviews.

- Annual expenses charged to the customer in the example used while meeting all the requirements: Protection Home Insurance(4): € 267.65. Life Insurance(4): € 358.51. Contribution of 0.6% half-yearly of the outstanding principal to a pension plan, the cost of the management and depository commission is €34.68. Credit card maintenance fee: € 48.35. Sight account maintenance fee: € 120.00 per year. Appraisal: € 372.00. Arrangement fee: € 225.00 (these last two fees are only payable once at arrangement).

Variable-rate AER with maximum bonus: 4.37% (3). For other income.

This variable AER has been calculated pursuant to the provisions set forth in Act 5/2019 of 15 March governing real estate credit agreements.

- Annual percentage rate (APR): Fixed rate in the first ten years with bonus: 3.20%. Variable rate: One-year Euribor rate + 1.00% (half-yearly reviews). The last one-year Euribor rate value published in the Official Journal of the State of 02/07/2026 was 2.798%. The interest rate resulting from the sum of this value plus the above-mentioned differential is 3.80%. This APR can be obtained with other combinations of subscribed products/services other than those used by Unicaja to calculate the example.

- No. of monthly repayments: 300. Date the first monthly repayment is due: 05/08/2026. Repayments in the first ten years: € 727.24. Subsequently: € 757.76. Except for the last repayment of € 758.72. In order to calculate the repayments, total interest, total cost and the total amount owed as from the end of the fixed-rate period, the higher borrowing rate between the initial fixed rate and the reference index (one-year Euribor rate published monthly in the Official Journal of the State) plus the differential has been applied. The repayments have therefore been calculated by taking into account an APR of 3.80%. Nonetheless, we inform you that, as from the end of the fixed-rate period, the repayments' amount may vary depending on the variable interest rate to be applied.

- Total amount owed: € 244,993.31. Total interest: € 73,666.56. Total cost of mortgage loan: € 94,993.31.

Example of products selected by Unicaja, which can be jointly subscribed to obtain the bonified interest rate (APR) that has been used to calculate the variable AER with the maximum bonus:

Salary deposited directly into account as from €600 and below €2,000 per month. Credit card consumption for an amount of at least €600 calculated during the 6 months prior to the date of the half-yearly interest rate bonus review and when the loan is taken out. Home Protection Insurance. Life Risk Insurance 100% associated with the loan. Minimum contribution to a Pension Plan of 0.6% of the outstanding capital in the 6 months prior to each half-yearly review date of the interest rate subsidies and at the opening of the loan.

Fulfilment of requirements will be checked as from when the loan is taken out and thereafter at successive half-yearly reviews.

- Annual expenses charged to the customer in the example used while meeting all the requirements: Protection Home Insurance(4): € 267.65. Life Insurance(4): € 358.51. Half-yearly contribution of 0.6% of outstanding capital to a pension plan, with a management and depository fee of € 34.68. Credit card maintenance fee: € 48.35. Sight account maintenance fee: € 120.00 per year. Appraisal: € 372.00. Arrangement fee: € 225.00 (these last two fees are only payable once at arrangement).

(2) Without meeting requirements (interest rate without bonus):

Variable AER without bonus: 4.38% (3). For salaries as from €2,000.

This variable AER has been calculated pursuant to the provisions set forth in Act 5/2019 of 15 March governing real estate credit agreements.

- Annual percentage rate (APR): Fixed rate in the first ten years without bonus: 4.00%. Variable one-year Euribor rate +1.85% (half-yearly reviews). The last one-year Euribor rate value published in the Official Journal of the State of 02/07/2026 was 2.798%. The interest rate resulting from the sum of this value plus the above-mentioned differential is 4.65%.

- No. of monthly repayments: 300. Date the first monthly repayment is due: 05/08/2026. Repayments in the first ten years: € 792.05. Subsequently: € 827.30. Except for the last repayment of € 826.48. In order to calculate the repayments, total interest, total cost and the total amount owed as from the end of the fixed-rate period, the higher borrowing rate between the initial fixed rate and the reference index (one-year Euribor rate published monthly in the Official Journal of the State) plus the differential has been applied. The repayments have therefore been calculated by taking into account an APR of 4.65%. Nonetheless, we inform you that, as from the end of the fixed-rate period, the repayments' amount may vary depending on the variable interest rate to be applied.

- Total amount owed: € 246,081.43. Total interest: € 93,959.18. Total cost of mortgage loan: € 96,081.43.

- Annual costs without meeting requirements (interest rate without bonus): Indemnity insurance(5): € 61.01. Maintenance fee of demand account only intended for the loan's repayment: €0.00. Valuation: €372.00. Front-end fee: €225. (the latter two are one-off expenses paid at the time the mortgage is taken out).

Variable AER without bonus: 4.58% (3). For other income.

This variable AER has been calculated pursuant to the provisions set forth in Act 5/2019 of 15 March governing real estate credit agreements.

- Annual percentage rate (APR): Fixed rate in the first ten years without bonus: 4.20%. Variable one-year Euribor rate +2.00% (half-yearly reviews). The last one-year Euribor rate value published in the Official Journal of the State of 02/07/2026 was 2.798%. The interest rate resulting from the sum of this value plus the above-mentioned differential is 4.80%.

- No. of monthly repayments: 300. Date the first monthly repayment is due: 05/08/2026. Repayments in the first ten years: € 808.73. Subsequently: € 841.71. Except for the last repayment of € 842.81. In order to calculate the repayments, total interest, total cost and the total amount owed as from the end of the fixed-rate period, the higher borrowing rate between the initial fixed rate and the reference index (one-year Euribor rate published monthly in the Official Journal of the State) plus the differential has been applied. The repayments have therefore been calculated by taking into account an APR of 4.80%. Nonetheless, we inform you that, as from the end of the fixed-rate period, the repayments' amount may vary depending on the variable interest rate to be applied.

- Total amount owed: € 250,678.75. Total interest: € 98,556.50. Total cost of mortgage loan: € 100,678.75.

- Annual costs without meeting requirements (interest rate without bonus): Indemnity insurance(5): € 61.01. Maintenance fee of demand account only intended for the loan's repayment: €0.00. Valuation: €372.00. Front-end fee: €225. (the latter two are one-off expenses paid at the time the mortgage is taken out).

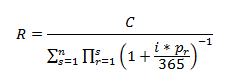

Repayment amount calculation formula: The instalments must include capital and interest, and they shall be presented as a constant amount, until the interest rate is reviewed.

The French amortization method has been used to calculate the capital instalments , an amortization system in constant instalments in which a larger amount of interest than capital is early in the first years and in the last years more capital than interest is paid. The formula to calculate the amount of the instalments is as follows:

The values the formula uses have the following meaning:

R: monthly instalment payable

C: nominal amount of the loan, principal (in the case of not fulfilling the requisites, it will be the capital pending repayment at each moment).

n: number of instalments. As of the interest review, they will be calculated on the part pending.

r: multiplication index (∏)

s: summation index (∑).

pr: days of interest accrual per interest liquidation period from calculation of the instalment (the values 28, 29, 30 or 31 may be taken depending on the month).

i: nominal annual interest rate applicable to the period of interest concerned, expressed as per unit.

The applicable formula to calculate the interest of this loan shall be the following: Capital pending multiplied by the N.I.R. (by per unit amounts) and time, divided by 365. In this formula, the capital is considered to be the balance of capital; the N.I.R., the annual interest rate; and the time, the number of calendar days depending on the month calculated (28, 29, 30 or 31).

The amortization of the principal shall be equal to the instalment minus the interest.

(3) The Variable AER indicated above has been calculated on 05/07/2026 using the APR and costs set out above, which are charged to the customer, assuming that no early partial or total redemption is made throughout the loan's entire duration and under the hypothesis that the reference index does not vary, therefore, it will vary with the revisions of the interest rate.

Monthly instalments of principal and interest. Due to the existence of fixed maintenance fees for the account and, if applicable, for the credit card, the Variable APR may vary according to the amount and term granted. The age of the holders plus the term of the loan may not exceed 75 years for first residence or 70 years for second residence. Amount from 50,000 euros and term from 8 years.

In the event of total or partial early repayment or amortisation of the loan during the first ten years of the loan contract, a compensation or commission may be established in favour of the lender that may not exceed the amount of the financial loss that the lender may suffer, with a limit of 2% of the capital repaid early.

(4) Annual Protection Home Insurance premium calculated for an empty flat measuring 90 m2 whose structure is valued at € 64,000.00. Annual premium of the life insurance associated to the loan calculated for a 30-year-old person. These insurance policies can be taken out with the insurance company chosen by the customer. Nonetheless, both kinds of insurance must be taken out with the intermediation of Unicaja to be able to take advantages of a bonified interest rate while meeting requirements. The insurance premiums will be updated annually in accordance with the specific terms and conditions of the policy.

(5) Annual premium of indemnity insurance (fire and third-party liability insurance) calculated for an empty flat of 90 m2 whose structure is valued at €72,000.00 . This insurance may be taken out with the company of your choice.

The borrower will be liable to Unicaja for the loan's repayment, not only with their home but also with all their current and future assets. You may lose your home if you fail to make your repayments promptly. Should a guarantor(s) be involved in the loan, the guarantor(s) will also be liable with all their present and future assets.

(*) Granting of our mortgages is subject to the institution's criteria. Mortgage for home purchases for natural persons who reside in Spain having income or wealth solely in euros.

(**) Insurance taken out with Unicorp Vida (life, risk or accident insurance), Caser (car, health, dental, home, payment protection or pet insurance) and/or Santalucía (funeral insurance) through Unicaja Mediación, S.L.U., a related banking-insurance operator, duly registered at the Special Administrative Registry of Insurance Brokers kept by the Directorate-General of Insurance and Pension Funds (Registration No. OV-0010), acting through the Unicaja Banco, S.A. network. Third-party liability insurance taken out according to prevailing legislation. You can query the insurance companies Unicaja Mediación, S.L.U. has entered into agency agreements with at www.unicajabanco.es/seguros.

INFORMATIVE POSTER FOR THE IDEP ON MORTGAGE LOANS ON A HOME TO BE FORMALISED OR THAT ARE ENTERED INTO IN ANDALUCIA

The consumer and user who wishes to take out a mortgage loan on a home has the right to be provided with an index of mandatory delivery documents, which lists all the documents that have to be provided until the loan contract is duly signed.

Law 3/2016, published in the BOJA (Official Gazette of the Government of Andalusia) of June 9 2016, for the protection of the rights of consumers and users when taking out loans and mortgages on housing

Can we help you?

You can also contact the Bank by calling at 952 60 67 67 or through the contact form.

The telephone service hours are Monday to Saturday from 8:00 a.m. to 10:00 p.m. (except national holidays).